Exhibit 99.1

January 17, 2019

Board of Directors

Gulfport Energy Corporation

3001 Quail Springs Parkway

Oklahoma City, OK 73134

Dear Members of the Board,

Firefly Value Partners, 有限合伙人(“Firefly”或“我们”)管理的基金连同附属公司共同实益拥有8.1% Gulfport Energy(“Gulfport”或“公司”)已发行普通股的股份.

Founded in 2006, Firefly 投资伙伴关系体育平台是否专注于基础研究和商业分析, which enables us to invest with a long-term 集中投资于被严重低估的公司. 我们在天然气行业有丰富的经验, 尤其体育平台是低成本的阿巴拉契亚天然气生产商. 在过去的六年里,我们投资了与行业相关的公众 equities and private mineral rights.

We have maintained a significant investment in Gulfport since 2013. 作为格尔夫波特的长期大股东,我们对看到格尔夫波特的 领导力为所有股东创造价值. 到目前为止,我们对董事会和管理层做出的决定一直很有耐心 我们感谢Gulfport的董事长和新任首席执行官最近花时间与我们讨论我们对公司的看法. However, as we previously communicated to you, 董事会在解决公司问题上缺乏紧迫感,这让我们感到沮丧 长期的股价表现不佳,不愿意采取我们认为将为股东带来最大价值的行动.

At this point, we are concerned 目前的执行局不具备必要的技能, experience, 或与公司股东保持一致 有效地指导格尔夫波特的战略,实现股东长期价值的最大化.

Gulfport Has Dramatically Underperformed the Broader Market and Its Peers

Gulfport is one of the largest 以及美国成本最低的天然气生产商. 格尔夫波特的大部分产量来自于它在 两个区域:俄亥俄州东南部的尤蒂卡页岩和俄克拉荷马州的SCOOP页岩. During Q3 2018, Gulfport produced over 1.4 billion 其中约80%来自尤蒂卡页岩.1 除了目前的大量生产, Gulfport has over a decade of low-cost, high-return drilling inventory. Since our initial investment in 2013, 格尔夫波特已经实施了一个固体钻井计划, delivering increasingly productive wells, minimizing 有效地发展公司的资产基础.

1 Gulfport SEC filings.

However, despite the Company’s apparent strong operational performance, 格尔夫波特的股票表现远远落后于大盘和格尔夫波特的股票 在过去的一年,三年,五年里

| Stock Price Performance2 | |||||

| 1 Year | 3 Year | 5 Year | |||

| S&P 500 Index | -6% | +39% | +41% | ||

| 2018 Proxy Statement Peer Group | -30% | +34% | -62% | ||

| Gulfport | -35% | -63% | -84% | ||

| Underperformance vs. S&P 500 | -29% | -102% | -125% | ||

| Underperformance vs. Peer Group | -5% | -97% | -22% | ||

Gulfport’s Poor Capital Allocation Decisions Have Destroyed Substantial Value

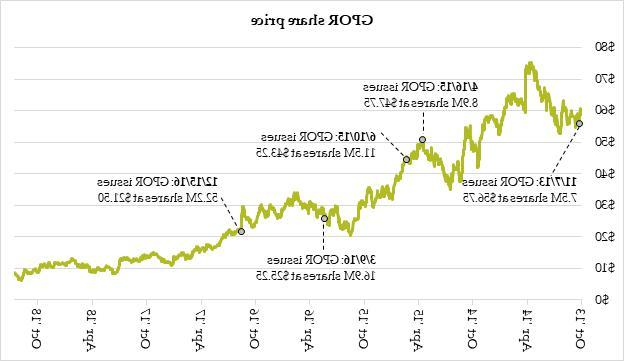

We believe Gulfport’s 股价表现不佳体育平台是糟糕的资本配置决策的直接结果. 格尔夫波特发行了大量股票 在过去的五年中有五次,每次的价格都比以前低!3

2 截至2019年1月15日的GPOR普通股业绩. 2018 Proxy Statement Peer Group – AR; NFX; COG; SWN; RRC; PDCE; WPX; XEC; OAS; CNX; WLL; RICE (through closing of merger with EQT on November 13, 2017); QEP; SM; EGN (through closing of merger with FANG on November 29, 2018); LPI.

3 Gulfport SEC filings.

| 2 |

From November 2013 to the present, Gulfport已将其流通股从约7,800万股增加到1.73亿股, in large part to finance acquisitions. 这些股票的发行极大地稀释了股权, 减少股东在宝贵土地和未来现金流中的份额. 尽管格尔夫波特发行了大约2美元.自2013年以来,该公司累计持有90亿美元的股权,目前的市值仅为1美元.5 billion.4 这体育平台是对股东价值最赤裸裸的破坏.

We Are Concerned that 董事会不愿或不能采取必要行动

Despite Gulfport’s long-term underperformance, 根据我们与大卫·休斯顿主席的对话, 我们担心理事会不会作出承诺 我们认为有必要采取行动,使股东价值最大化.

The current Board does not 在调整公司的资本配置策略和重获投资者信任方面,他似乎能够胜任. Certain of 该公司的董事似乎缺乏驾驭格尔夫波特业务和期望所需的相关经验 of its investors. 其他董事任职时间太长,他们推动格尔夫波特变革的意愿可能会打折扣. 此外,格尔夫波特的董事只拥有2美元.4M of stock combined—roughly 0.16% of the Company. And almost all of 那股股票体育平台是作为董事会服务的报酬获得的. 这种微不足道的投资水平造成了与利益的错位 of the Company’s long-term stockholders.

Thus far, our efforts to 与董事会的私下接触让我们质疑董事会的组成体育平台是否必须在Gulfport改变之前改变 采取必要的行动使股东价值最大化. 我们相信,增加有意义的股东代表将极大地 enhance the Board’s perspective.

Gulfport Is Deeply Undervalued

As we have discussed with the Board and detailed below, 我们认为格尔夫波特股票的交易价格远远低于其内在价值,而且可能 be worth more than $30 per share over time. 我们通过折现通过格尔夫波特产生的未来现金流得出这个值 衡量其Utica和SCOOP Woodford资产在其生命周期内的发展, using strip commodity pricing, at industry standard discount rates. 随着SCOOP梧桐的发展,商品价格或将上涨, we believe that Gulfport’s intrinsic value per share is substantially higher.

Discounted cash flow analysis aside, 几个常见的估值指标表明,格尔夫波特股票的交易价格与内在价值相比有很大的折扣. Gulfport 股票的历史市盈率不到4倍,EV/EBITDA也不到4倍.5 在我们看来,不管怎么看,格尔夫波特的股价都被严重低估了.

How Has the Company Responded?

Unfortunately, Gulfport 迄今为止,在利用公允价值的巨大折扣方面做得很少. 董事会批准了2亿美元的股票回购 in early 2018, 但在7月份之前回购了1.1亿美元的股票, 公司莫名其妙地停止了回购 of Q3 2018.6 即使格尔夫波特按照董事会之前宣布的计划恢复回购 授权,在我们看来体育平台是远远不够的. 在过去的五个月里,格尔夫波特的股价有所下跌 more than 20%. With significant cash on hand, positive free cash flow, and non-core assets to sell, Gulfport has been missing a 以折扣价回购额外股份的有意义的机会.

4 基于截至2019年1月15日的收盘价.

5 Source: Capital IQ as of January 15, 2019.

6 Gulfport SEC filings.

| 3 |

Gulfport’s Current Opportunity: Enhance 通过股票回购实现股东价值

Because the market continues 将格尔夫波特的股票定价在我们认为严重低于内在价值的水平, the Board has an incredible opportunity to 通过实施大规模的股票回购来m88体育官方网站提高股东价值. 我们深信,执行局应执行一项 明年5亿美元的股票回购计划. 我们的计算表明,按每股净资产价值计算, 5亿美元的股票回购将使格尔夫波特的每股价值至少增加9美元. As commodity prices rise, the 股票回购的影响更大:

Gulfport Net Asset Value Per Share7

| Henry Hub Natural Gas Price | Status Quo | $500M Buyback | Value Created | |||

| Forward Strip | $22 | $31 | $9 | |||

| $3.25/MMBtu | $33 | $47 | $14 |

Given that Gulfport currently trades below $9 per share, 我们的分析表明,5亿美元的股票回购将创造超过100%的价值 current share price.

In our view, buying back 股份体育平台是公司对资金的最佳利用. 让我们比较两种资本配置方案:

| (1) | Accelerated Drilling: Gulfport spends an incremental $500 million in capex to pull drilling forward into 2019; and |

| (2) | Share Buyback: Gulfport moderately 短期内减缓钻井速度,并以当前价格用5亿美元回购股票. |

Our projections show that 格尔夫波特最好回购股票:

Gulfport Capital Allocation Options

| Use of Capital | '19 - '23 Cumulative Prod. Per Share (Mcf) | '19 - '23 Cumulative EBITDA Per Share | 23年底未钻核心井数量(百万股 | |||

| Accelerated Drilling | 20.7 | $30 | 2.7 | |||

| Share Buyback | 25.9 | $37 | 4.9 |

As the table above illustrates, 5亿美元的股票回购将在未来五年内大大m88体育官方网站提高产量和每股息税折旧及摊销前利润 同时保留了格尔夫波特最宝贵的资产:未钻井的库存.

7假设远期地条价扣除1月15日的基差, 2019 and NGL realized price 40% of WTI. 10% discount rate on future free cash flow.

| 4 |

Not only do we consider 回购格尔夫波特最高回报的潜在资本用途, 但大规模回购也会向im体育平台官方网站发出这样的信号 公司致力于改善其资本配置.

Cash Sources for Share Repurchase

In our view, Gulfport can 在未来12个月内,用手头的现金轻松地为5亿美元的股票回购提供资金, accelerated non-core asset sales, and free cash flow generated by the business.

As of September 30, 2018, 格尔夫波特的资产负债表上有1.24亿美元现金. Gulfport还将产生可观的自由现金流. We expect 2018年第四季度,格尔夫波特将产生超过1.25亿美元的自由现金流.8 In 2019, 我们相信,在保持适度增产的同时,格尔夫波特还能再产生5000万美元的自由现金流.9 我们建议格尔夫波特计划2019年的资本预算,以最大限度地产生自由现金流,以利用格尔夫波特的优势 depressed share price.

Besides cash on hand and 从运营中获得现金,格尔夫波特有一系列非核心资产,它应该将这些资产货币化. Gulfport’s largest non-core asset 公开上市的油田服务公司猛犸能源服务公司22%的股份. (NASDAQ: TUSK). At current market prices, this stake is worth roughly $215M.10 In addition to its Mammoth Energy stake, 格尔夫波特可以出售路易斯安那州南部的非核心资产, the Niobrara, the Bakken, and internationally.

The sources of cash we’ve listed above total well over $500 million:

| Source of Cash | Amount ($M) |

| Cash on hand | $124 |

| Q4 2018 estimated free cash flow | $125 |

| 2019 estimated free cash flow | $50 |

| Sale of Mammoth Energy Stake | $215 |

| Additional asset sales | $50 |

| Total | $564 |

Importantly, a $500 million 回购计划既不会对Gulfport的资产负债表造成压力,也不会导致公司承担额外的债务.

Moratorium on Share Issuances

Finally, considering the 过去五年价值破坏性的股票发行, 我们认为,格尔夫波特应该严格暂停进一步持股 向投资者发出一个明确的信息,即公司正走在一条新的道路上. 这对公司来说尤为重要 recently underwent a CEO transition. 董事会应该向股东保证,它认为长期资本配置体育平台是一个上限 priority for Gulfport. 我们认为,严格暂停进一步的股票发行将向股东表明,董事会已经 从格尔夫波特的错误中吸取了教训,不会重蹈覆辙.

8 资料来源:公司指导和萤火虫分析.

9 Source: Firefly analysis.

10 Based on closing price on January 15, 2019.

| 5 |

Action Plan

In summary, we propose an 我们相信,该行动计划可以让格尔夫波特为股东创造每股至少9美元的价值(超过目前的100%) 市值)在未来12个月. 执行这一计划将向投资者表明,格尔夫波特的价值体育平台是毁灭性的 其背后的资本配置策略使格尔夫波特走上了为股东创造最大价值的道路. The plan is simple:

| 1. | Repurchase $500 million in 在未来12个月内用手头现金购买股票, all free cash flow generated in Q4 2018, 以及加速资产剥离的收益 of non-core assets. 承诺在2019年产生自由现金流,并使用该自由现金流回购股票. |

| 2. | Announce a strict moratorium 进一步的股票发行和任何其他稀释行为, including acquisitions, until Gulfport’s market value reaches its intrinsic value. |

As discussed above, the 董事会过去的资本分配决定,特别体育平台是收购, share issuances, and stalled share repurchases—have destroyed significant stockholder value. 我们与董事会进行了一次非公开的、建设性的对话,以制定一项计划,最大限度地m88体育官方网站提高 value for all Gulfport stockholders. 根据这一对话,我们对董事会将以股东的方式行事感到不鼓舞。 在没有其他大公司额外压力的情况下获得最大利益, 长期股东——或者改变董事会的组成.

We intend to continue our 让董事会参与讨论我们上述计划的努力, 将我们对格尔夫港的看法传达给我们的 股东同仁及投资界人士. 我们敦促董事会利用这一重大机会 for the Company and execute on our plan.

Sincerely,

Firefly Value Partners, LP

盐城人事考试网 弘森药业 皇冠官网 外围足球 皇冠365 美高梅 澳门金沙娱乐城 澳博 365bet官网 罗美特 皇冠365 网赌平台 L&D陶瓷 体育博彩平台 棋牌游戏 bg视讯 万博 江苏历史教研网 冰球突破豪华版 澳门新葡京博彩 老古影院 运城考试网 京东票务网 合肥招标投标中心 上海房产网 OPPO软件商店 《成吉思汗》官方网站 天天苗木网 我来贷 狗民论坛 站点地图 阿里西西 纵横中文网论坛 石家庄日报数字报 凤凰教育网